For plumbers, roofers, electricians, joiners and builders across the UK, a van is not just a vehicle, it is the backbone of the business.

It carries your tools, materials, branding and reputation from job to job.

Despite this, one of the most common financial mistakes tradespeople make is paying large sums of cash upfront for vans without fully considering how this impacts their cashflow, growth potential and tax position. In 2026, with vehicle prices remaining high and operating costs rising, the decision between business van finance and buying outright is more important than ever. This guide breaks down both options clearly so you can make the smartest financial decision for your trade business.

Quick Answer: Is It Smarter to Finance a Van or Buy Outright in 2026?

For most UK trades businesses, financing a van is the smarter option in 2026. Using business van finance allows you to preserve cash within your company, maintain stronger working capital, spread the cost of the vehicle in a predictable way and benefit from potential tax efficiencies. Buying outright may suit some businesses with excess cash and no growth plans, but in many cases it restricts flexibility and slows down expansion.

The right choice depends on how you want your business to operate over the next few years rather than simply how much money you have available today.

Buying a Business Van Outright: The Pros and Cons for Trades

Buying a van outright can feel appealing because you own the vehicle immediately and do not have any monthly payments or finance agreements to manage. For some tradespeople, especially those who dislike ongoing commitments, this can provide peace of mind and a sense of simplicity in their finances. It can also make accounting feel more straightforward in the short term, as there are no interest charges to factor in.

However, the downside of buying outright is that it requires a significant upfront cash payment, often running into tens of thousands of pounds. That cash then becomes tied up in a depreciating asset, which means it is no longer available to support your business operations. Many trades underestimate how valuable working capital is, particularly when it comes to funding new tools, covering staff costs, paying for marketing or simply having a buffer for quieter months. By using a large lump sum to buy a van outright, you may be limiting your ability to grow, invest and respond to opportunities as they arise.

Business Van Finance: A More Flexible Approach for Growing Trades

Business van finance allows tradespeople to access reliable vehicles while keeping their cash available for day-to-day operations and growth. Instead of paying a large amount upfront, you spread the cost over manageable monthly payments, which makes budgeting far more predictable. This approach also makes it easier to upgrade vehicles as your business grows, ensuring your vans remain reliable, professional-looking and compliant with any future regulations.

From a cashflow perspective, finance can significantly reduce financial pressure. Rather than draining your reserves in one go, you can keep money available for essential investments such as specialist tools, additional labour or marketing that generates new leads. In many cases, using finance strategically allows trades to grow faster because they are not constrained by the need to save large sums before upgrading or expanding their fleet. While finance does involve interest and ongoing payments, the trade-off is often improved flexibility and stronger overall business health.

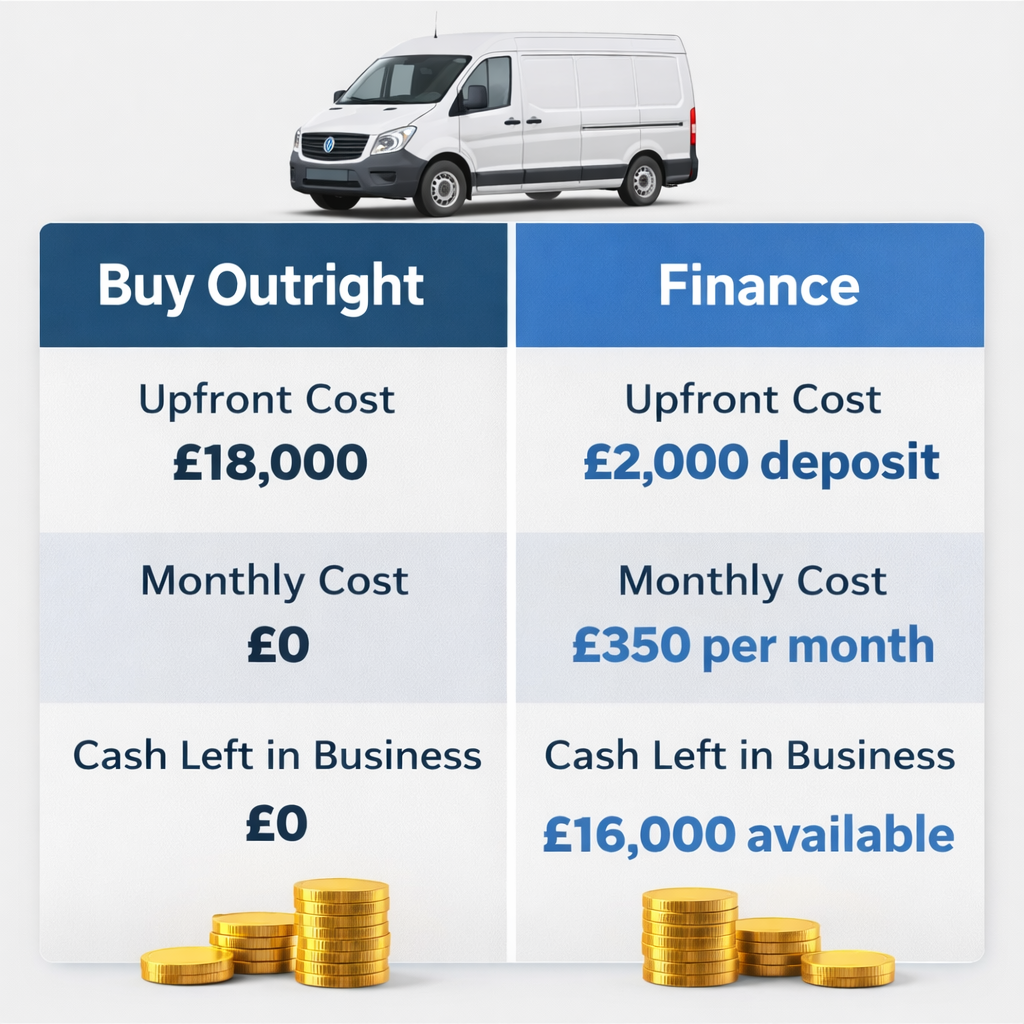

Real-World Cost Comparison: Finance vs Buying Outright

To understand the difference in practical terms, consider the scenario of purchasing a used van for £18,000. Buying outright means that entire £18,000 leaves your business immediately, leaving no cash available from that sum to support operations or growth. Financing the same van might require a smaller deposit followed by manageable monthly payments, allowing you to retain a significant amount of cash within your business. That retained cash could then be used to purchase tools, fund advertising, cover wages or create a safety buffer for quieter periods. While both options ultimately provide you with a van, the financial position of your business after the purchase can be dramatically different.

Tax Considerations for UK Trades in 2026

Tax treatment is an important factor when deciding whether to finance a van or buy outright. While you should always confirm the specifics with your accountant, many UK trades can benefit from tax efficiencies when using business van finance.

Monthly finance payments can often be offset as allowable business expenses, and in some cases VAT may be reclaimable depending on how the vehicle is used and the structure of your business. Buying outright typically involves claiming capital allowances, which can be beneficial but may not offer the same level of flexibility in managing cashflow and tax planning.

The key difference is that finance can smooth both your expenses and your tax position over time, rather than concentrating the financial impact into one large payment.

How Lenders View Finance vs Cash Purchases

Many tradespeople assume that lenders prefer businesses that avoid finance and pay for assets outright, but in reality, lenders often view structured finance positively. Businesses that use finance sensibly demonstrate an understanding of cashflow management and long-term planning.

Maintaining cash reserves while spreading asset costs can actually strengthen your overall financial profile, making it easier to secure funding for future investments. In contrast, depleting cash reserves to purchase vehicles outright can make your business appear less financially resilient, which may impact future borrowing options.

When Buying Outright Might Still Make Sense

There are situations where buying a van outright can be the right decision. If your business has surplus cash that is not required for growth, marketing or staffing, and you prefer not to have any ongoing finance commitments, purchasing outright can offer simplicity. It may also suit trades with stable workloads and minimal expansion plans. However, it is important to ensure that this choice is made strategically rather than emotionally.

The decision should be based on what supports the long-term health and flexibility of your business, not simply on a preference to avoid finance.

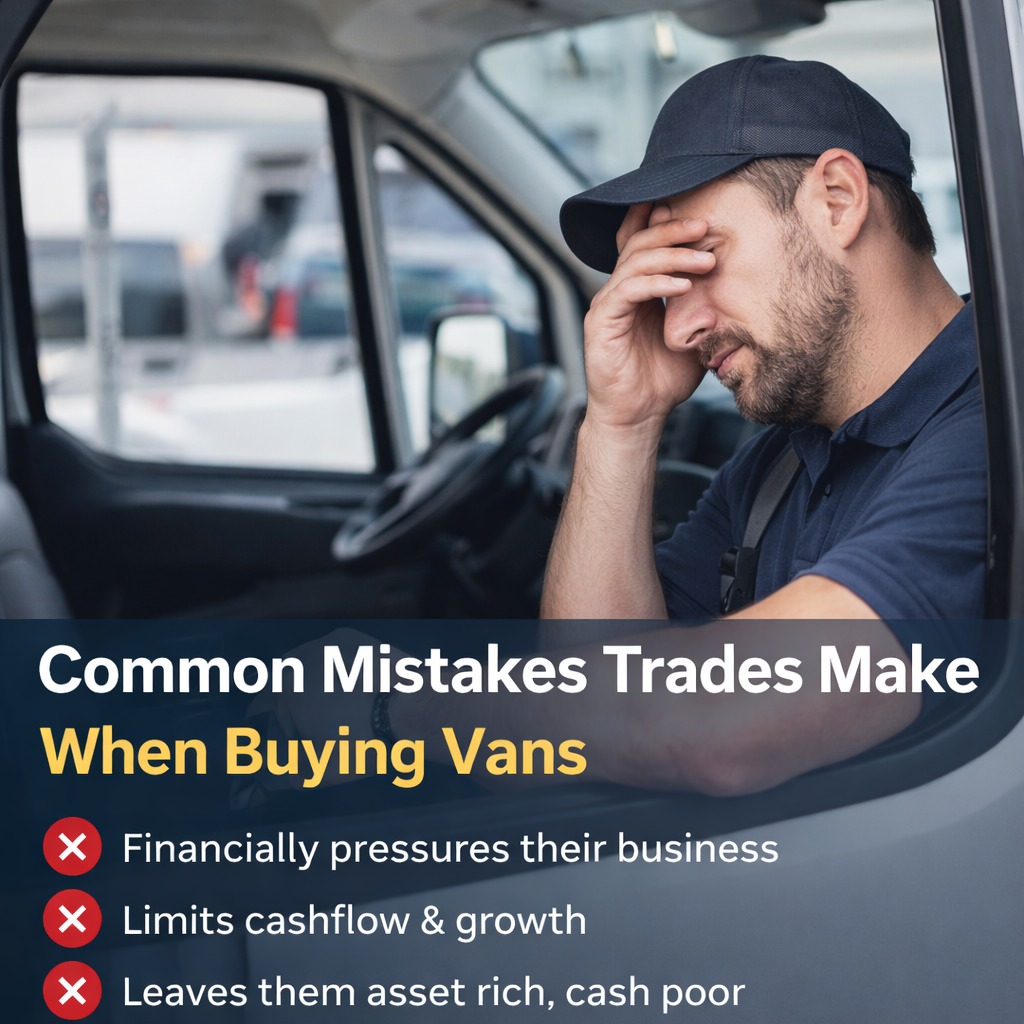

Common Mistakes Trades Make When Buying Vans

One of the most common mistakes tradespeople make is rejecting finance purely because they associate it with personal debt or financial risk. In business, finance is a tool, and when used properly, it can be a powerful way to support growth. Avoiding finance at all costs often leads to businesses becoming asset-rich but cash-poor, which can create unnecessary pressure and slow down progress. The most successful trades treat finance as part of their overall business strategy rather than something to be avoided.

Frequently Asked Questions

FAQs: Business Van Finance vs Buying Outright (UK Trades, 2026)

Is it better to finance a business van or buy outright in the UK in 2026?

For most UK tradespeople in 2026, financing a business van is usually better than buying outright because it protects cashflow, spreads the cost of the vehicle over time and keeps working capital available for tools, wages and growth. Buying outright can suit businesses with surplus cash and no growth plans, but for growing trades, van finance is typically the smarter long-term option.

Can UK tradesmen get business van finance with bad credit or limited trading history?

Yes, UK tradesmen can still get business van finance with bad credit or limited trading history by using specialist lenders. Many finance providers work with sole traders and limited companies that have CCJs, low credit scores or are newly trading. Using a specialist broker improves approval chances and helps secure more suitable terms.

Is business van finance tax deductible in the UK?

Business van finance is often tax deductible in the UK because monthly payments can usually be claimed as allowable business expenses, and VAT may be reclaimable depending on how the van is used and the business structure. The exact tax treatment depends on whether you are a sole trader or limited company, so you should always confirm with your accountant.

Does buying a van outright affect cashflow for UK trades?

Yes, buying a van outright can significantly affect cashflow for UK trades because it removes a large lump sum of money from the business at once. This reduces the cash available for marketing, tools, staff wages and emergency costs, which can limit business growth and flexibility.

What is the cheapest way to get a business van in the UK?

The cheapest way to get a business van in the UK is not always buying outright. While paying cash avoids interest, financing a van can be more cost-effective overall because it preserves cashflow, allows tax efficiencies and enables businesses to invest in growth. The best option depends on your business finances, growth plans and tax position.

Is business van finance better for limited companies or sole traders?

Business van finance works well for both limited companies and sole traders in the UK. Limited companies may benefit from additional tax efficiencies, while sole traders benefit from preserving cashflow and spreading costs. The best structure depends on income, tax position and future growth plans.

Will financing a van hurt my chances of getting future business finance?

No, financing a van responsibly can actually improve your chances of securing future business finance. Lenders often view structured finance as a sign of good financial management, especially when payments are made on time and cashflow is maintained. Using finance sensibly can strengthen your business credit profile.

Should trades buy used vans outright or finance newer vans?

For many UK trades, financing a newer, more reliable van is often smarter than buying an older van outright. Newer vans reduce downtime, improve brand image and often come with warranties, while finance allows you to access better vehicles without draining your business cash reserves.